How Broadcom Makes Money

Q1 2026 Earnings Overview

Broadcom: The AI Networking Boom Meets the Enterprise Cash Cow

Broadcom just delivered a Q1 2026 earnings report that perfectly encapsulates CEO Hock Tan’s legendary playbook. If you want to understand what a masterclass in capital allocation and operational ruthlessness looks like, look no further than this quarter’s numbers.

While much of the market’s attention has been fixated on companies building large language models, Broadcom is quietly taxing the entire ecosystem. They are operating essentially as two monopolies in a trench coat: one supplying the critical custom silicon and networking gear needed to build AI data centers, and the other acting as an inescapable tollbooth for enterprise software infrastructure.

The result? A staggering $22,187 million in total revenue, paired with the kind of profit margins that most software companies can only dream of.

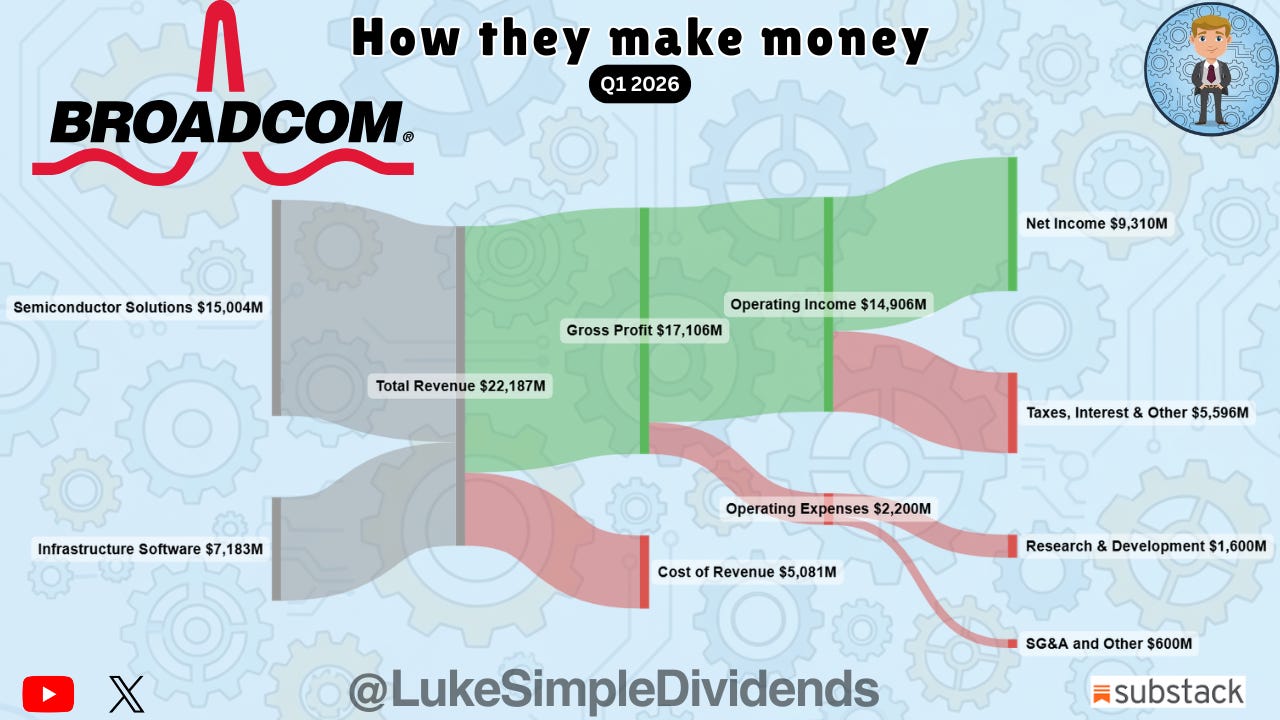

📊 The Income Statement Breakdown

The Top Line: A Two-Headed Monster

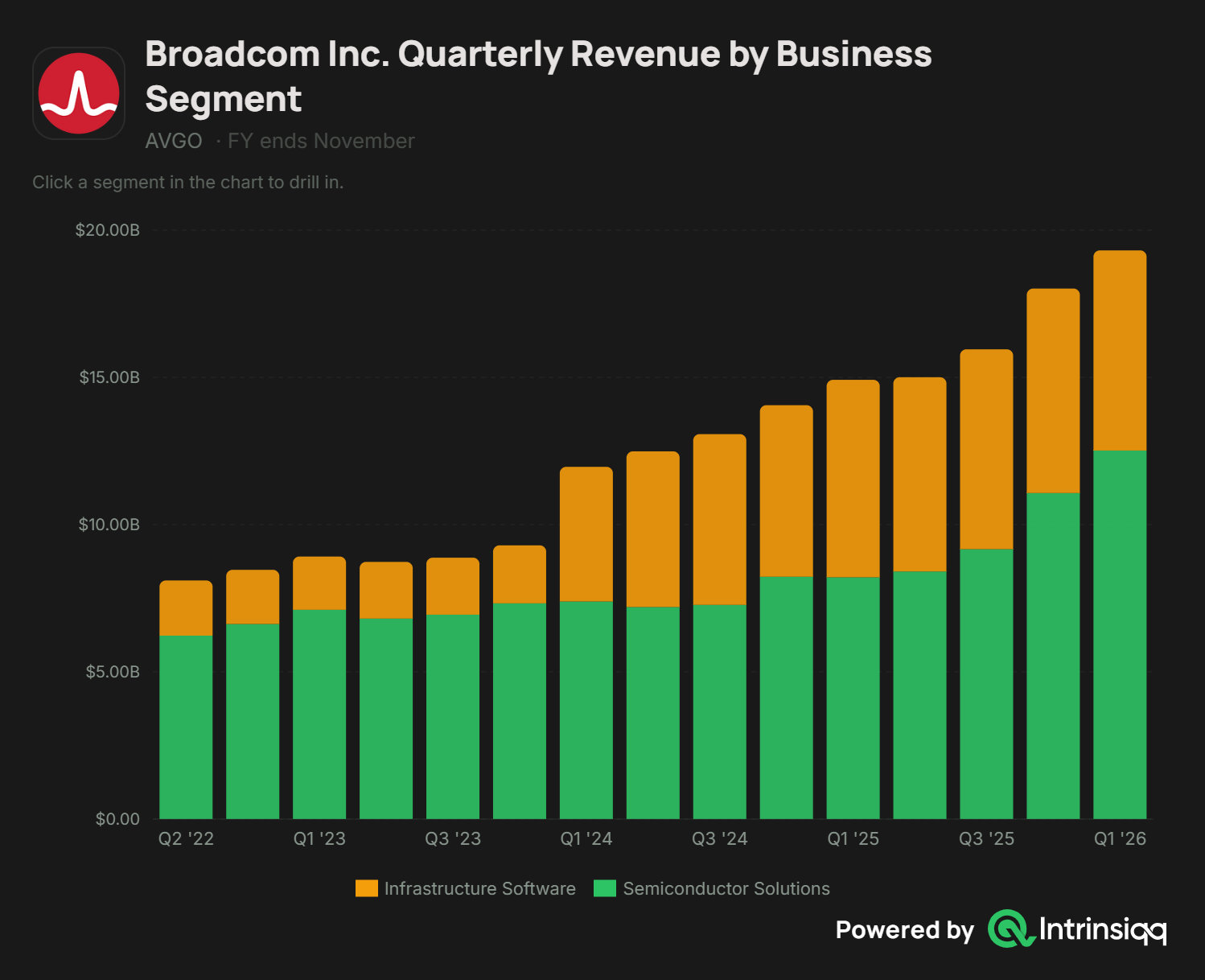

Semiconductor Solutions: $15,004 million (67.6% of total revenue)

Infrastructure Software: $7,183 million (32.4% of total revenue)

Broadcom’s revenue mix is beautifully balanced. The Semiconductor Solutions segment ($15.0 billion) is the tip of the spear right now. While Nvidia dominates the GPU space, those GPUs are practically useless unless they can talk to each other at lightning speeds. Broadcom dominates the high-end AI networking space (with their Tomahawk and Jericho switches) and the custom ASIC market (building specialized AI chips like Google’s TPUs). As AI clusters scale from tens of thousands to hundreds of thousands of chips, Broadcom’s networking revenue scales right alongside them.

The Infrastructure Software segment ($7.2 billion) represents the culmination of Broadcom’s aggressive M&A strategy, heavily supercharged by the integration of VMware. This side of the business isn’t about hyper-growth; it is about locking in the world’s largest enterprises into long-term, high-margin subscription contracts.

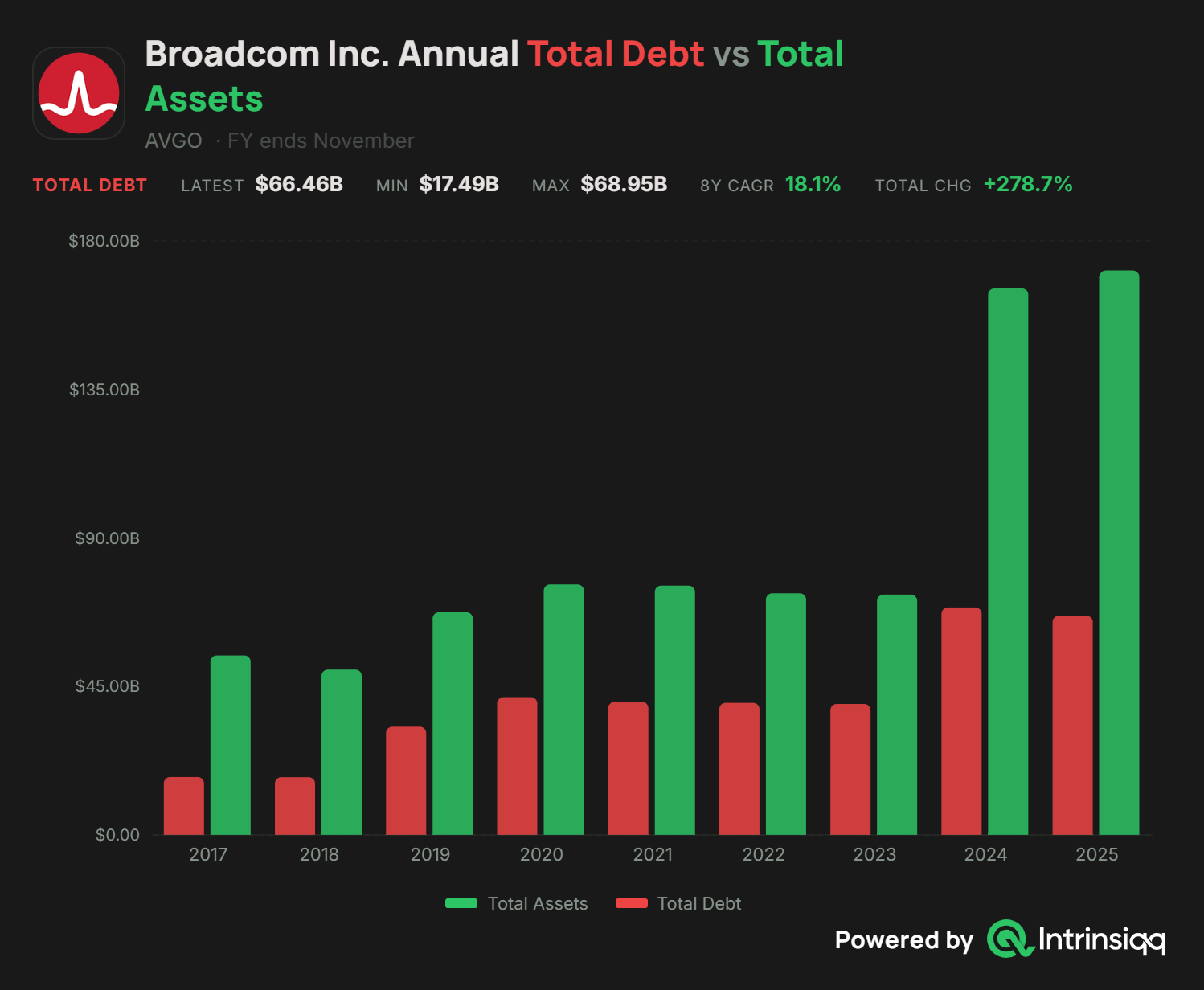

Total Debt vs. Total Assets

Why it matters: Broadcom grows by buying massive companies (CA Technologies, Symantec, VMware) using debt. A balance sheet chart proves to investors that while their debt load spikes after an acquisition, their ballooning asset base and cash generation safely support it.

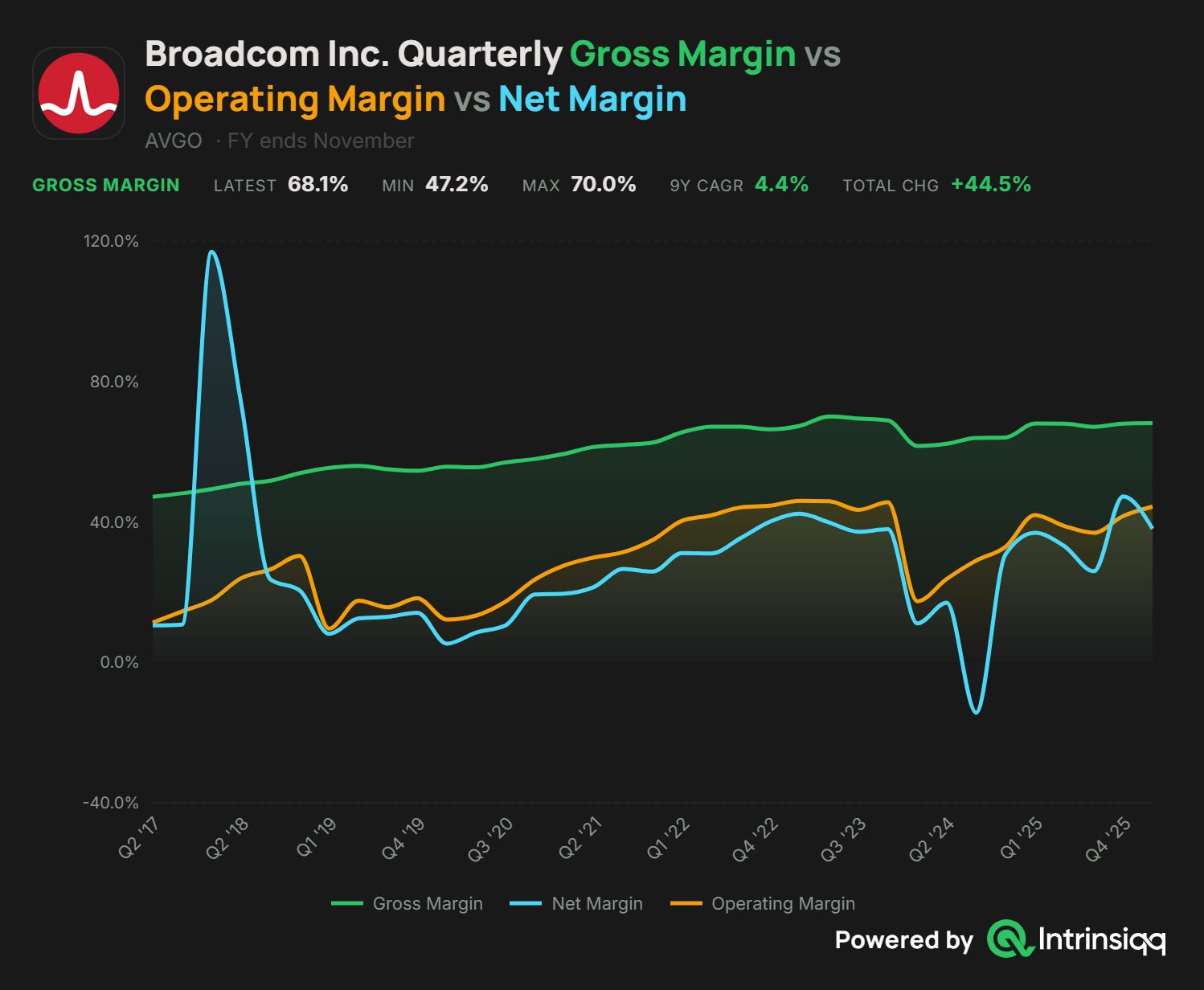

The Profitability Engine

Gross Profit: $17,106 million (77.1% Gross Margin)

Operating Income: $14,906 million (67.2% Operating Margin)

Net Income: $9,310 million (42.0% Net Margin)

This is where the Hock Tan magic becomes mathematically undeniable. Broadcom generated a 77.1% gross margin on a business that still involves manufacturing physical silicon.

But the real story is the operating expenses. To generate that $22.2 billion in revenue, Broadcom spent only $2,200 million in OpEx.

Research & Development (R&D): $1,600 million

SG&A and Other: $600 million

Look closely at that SG&A number. Broadcom spends just 2.7% of its revenue on Sales, General, and Administrative costs. That is almost unheard of in the tech industry. This happens because Broadcom does not waste money on massive marketing campaigns or bloated middle management. They strip acquired companies down to the studs, eliminate duplicate corporate overhead, and sell directly to the top 600 global enterprises and cloud hyperscalers who literally cannot operate without their tech.

The Bottom Line: Broadcom is a cash-printing machine. After paying a massive $5,596 million in taxes, interest on their acquisition debt, and other expenses, they still dropped $9.3 billion straight to the bottom line. It is a dual-engine business model where AI hardware funds the debt payments, and enterprise software funds one of the most reliable dividend payouts in the tech sector.

Connect with Me Live

📱 Want to see my moves in real-time?

I post all of my live buys and sells as they happen. Follow my journey and see my trades directly on Blossom and X / Twitter.